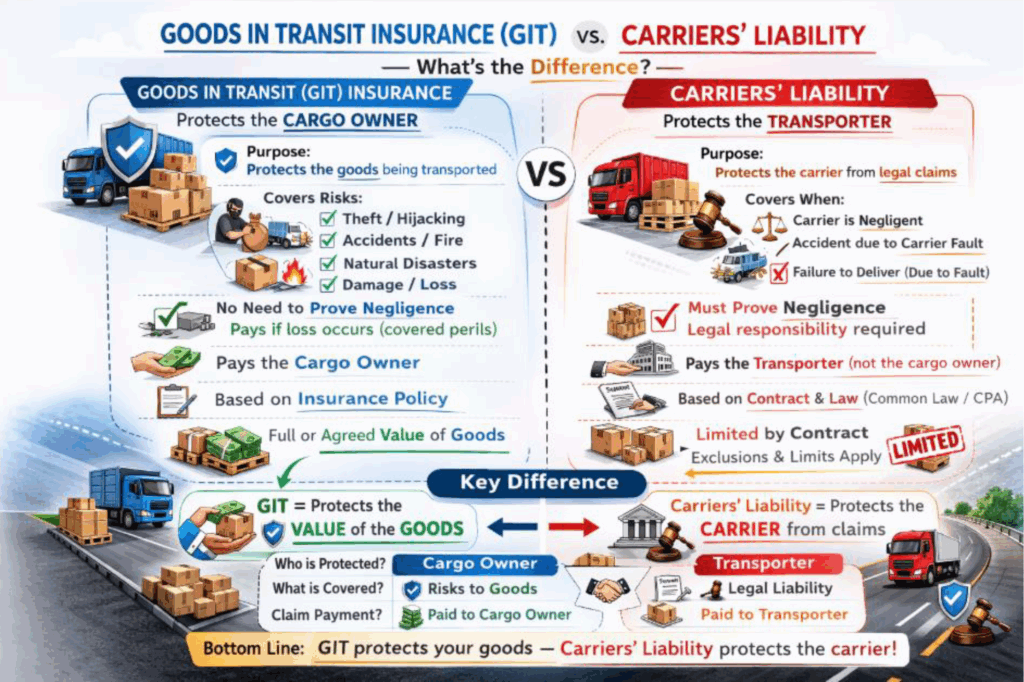

In the road transport and logistics industry, there is often confusion between Carrier’s Liability Insurance and Goods in Transit (GIT) Insurance.

Often, we will hear customers proclaiming that their goods are comprehensively insured under the transporter’s insurance policy or they will be insistent that the transporter has an automatic insurance policy in place that covers their goods.

It is critical that consignors of freight know and understand the difference between Carrier’s Liability insurance and Goods in Transit (GIT) insurance.

Carriers Liability insurance is there to protect the carrier (the transporter) from claims where there has been an incident in the freight operation that has resulted in loss or damage to consignors’ freight through an act of negligence.

The policy does not protect the consignor (sender) or owner of the freight; it protects the transporter in the event that a potentially negligent action has caused loss or damage to the freight.

Let’s look at an example.

Terry’s Electronics in Johannesburg ships R180,000.00 worth of electronic equipment to a customer in Durban using a road freight company.

The transporter has a Carriers Liability policy with its insurer.

The Transporter collects the freight and issues a waybill that refers to their terms and conditions of carriage which state that:

- The carrier is not responsible for loss or damaged caused by events beyond its control like hijacking, vehicle overturning, fire etc.

Goods are carried subject to the carrier’s standard terms and conditions of contract, which exclude acts of negligence. (Carriers cannot contract out of gross negligence, but they can contract out ordinary negligence.)

During the journey, the truck is hijacked on the N3, and all the goods on the vehicle are stolen. Terrys Electronics, the consignor, will not succeed in making a claim against the Carrier or the Carrier’s Insurer, because the Carrier’s Liability Policy will not respond to this event. The Transporter is not legally liable.

Terrys Electronics will be out of pocket for the full value of the shipment of R 180,000.00

Goods in Transit Insurance.

Goods in transit insurance is there to protect the consignor, not the freight operator. The consignor is the insured; he has declared the value of the consignment to the insurer and paid a premium based on this value to the insurer.

The perils that the G.I.T policy will respond to, will depend upon the Policy wording but generally it will cover risks such as, theft or hijacking, fire, vehicle overturning, flood damage etc.

GIT insurance does not require the cargo owner to prove that the transporter committed a negligent act or was at fault. If the insured event occurs and the goods are covered under the policy, the insurer compensates the cargo owner.

This makes GIT insurance a much more comprehensive form of protection for the value of the goods.

The fundamental difference between the two can be summed up by answering the following questions:

Carrier’s Liability asks: “Did the transporter perform an act of negligence and is therefore legally responsible?”

Goods in Transit insurance asks: “When the cargo was lost or damaged during transit, was this caused by an event that is covered in the policy wording?”

Understanding the distinction between the two forms of protection is essential for any consignor that ships valuable freight. Because when something goes wrong on the road, the difference between the two can determine whether a business recovers from the loss or is financially stressed by having to absorb that loss in its entirety.